Newsletter: Diversification is Not Dead

(Written 2019. For illustration only)

Diversification has been equated as “the only free lunch” in investing. That is, by placing your bets in many assets with low correlations you can not only reduce the volatility of your portfolio, but also reduce the risk of significant losses. But from January to August 2019 stock and bond markets have both produced extraordinary positive returns. This has raised concerns among many fund sponsors and investors. If all of my assets are up at the same time, has diversification lost its power? Does this mean that when the market corrects, they will all go down at the same time? At the extreme some market pundits are asking, “Is diversification dead?”

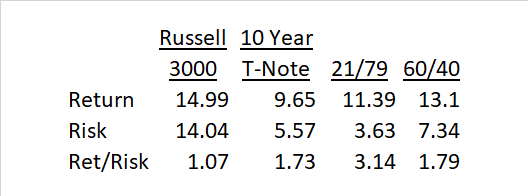

Fortunately, this is not the case. While both the stock and bond markets are up on a cumulative basis this year, they took different routes on their way up. There is an old saying among mathematicians that “correlation is not causality.” We can add to that saying, “cumulative returns are not correlation.” The fact is that this has been one of the best years for diversification. Both stocks and bonds have given strong positive returns with strong negative correlation. As a result, a portfolio of stocks and bonds would have produced strong returns as well but at low risk. The overall Return/Risk (or “Sharpe”) ratio of a balanced portfolio would be higher than either as well. That’s what diversification is about.

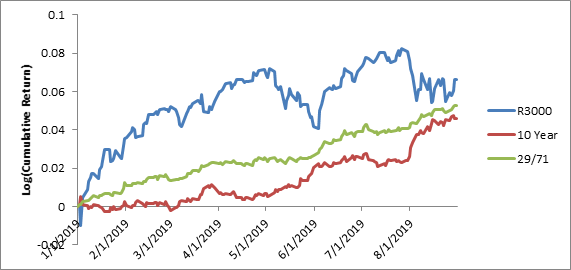

The chart below shows the cumulative returns of the Russell 3000 Stock Index and a continuous maturity 10 Year US T-Note. We show the charts in log space so the higher volatility of stocks doesn’t drown out the bonds. As you can see while they both ended up at a similar spot at the end of August, when stocks went up bonds tended to go sideways or down, and when bonds went up stocks were going down. In fact over this time period the daily correlation of the two assets was -59% which is even more negative than the -35% experienced over the last ten years. We can also state that this -59% correlation is similar across daily, weekly and monthly time scales.

Log Cumulative Returns: Jan – Aug 2019

The chart also shows a balanced portfolio of 21% stocks and 79% bonds. This is a typical low risk portfolio for retirees and splits risk (as defined by standard deviation) between stocks and bonds. The table below shows this balanced portfolio having a much higher Sharpe ratio than either stocks or bonds. The traditional 60/40 portfolio also has a higher return/risk ratio than either asset separately. While this analysis is on the US, other developed markets show very similar patterns.

January – August 2019

So we can ask, “What is the causation for this low correlation?” It appears stocks and bonds are up for different reasons. In 2019 it’s likely that participants in the stock and bond markets have been interpreting the same information differently. The stock market this year has been chronically optimistic (particularly in the US) especially after Jerome Powell, the Chairman of the Federal Open Market Committee, became more dovish and Fed began lowering interest rates. The stock market thought that was great news because cutting interest rates would stimulate the economy and avert a slow-down or recession. The bond market, however, was not that enthusiastic. In fact the bond market thought that if the Fed was worried enough about the economy to cut rates, then the economy must already be fragile and the risk of a slow-down or recession is higher than the stock market thinks. Chairman Powell and other Federal Reserve officials have sent signals in both directions citing a strong economy as well as risks to the economy. This difference of opinion in the two markets is the reason for the negative correlation.

Whether the bond or stock market is right is debatable, but they can’t both be right. In the end the economy will keep growing or it will slow-down. In either case one asset will continue to be up while the other will lose its gains. But diversification will still win out. A simultaneous retreat always possible, but it is not inevitable and the causation for such an event is missing.

So in the end diversification has not failed. It has not stopped working. Investors should not confuse positive cumulative returns with positive correlation. The underlying dynamics show that diversification is alive and well and will likely continue to work for investors when it’s most needed.